The majority of phone users from my generation will have at least heard of this App. It's a "cross-platform mobile messaging app which allows you to exchange messages without having to pay for SMS." The advantages it has over iMessage or BBM (now available on iPhone and Android) is that WhatsApp Messenger is available for iPhone, BlackBerry, Android, Windows Phone and Nokia. In addition to basic messaging WhatsApp users can create groups, send each other unlimited images, video and audio media messages. It now has around 500 million users world wide and of which 70% use the service everyday.

Before we go into the details as to why Facebook believed Whatsapp was worth the $19bn they paid, lets put in perspective how much that is. Three days ago the worlds most wanted man was arrested in Mexico, Joaquin Guzman. He has been listed on Forbes 100 richest men in the world (ranked 41st in 2009) and said to be worth $1bn. WhatsApp has now been sold for 19 times the value of him. When you're to think of it this way, considering the company had made only $20 million in sales last year, it's laughable. Is there a bigger picture?

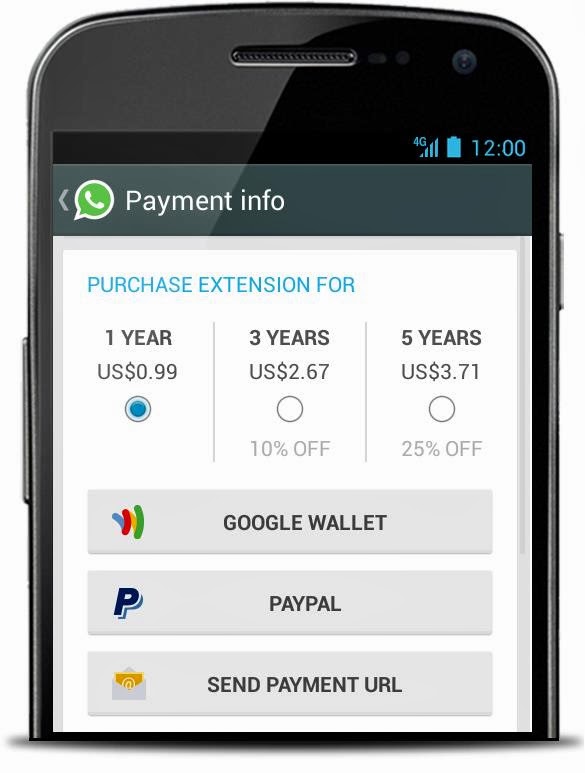

Mark Zuckerburg spoke on behalf of Facebook at a press conference in Barcelona yesterday and believes that WhatsApp is a "rare platform that has the potential to reach out to 1 billion mobile users". The real majesty of web dynamics and most obvious is the colossal global reach at nearly zero marginal costs. Whatsapp has around 50 employees. It has no marketing costs. No Washington lobbyists. No stores. No global campus. No sponsorship of the local symphony. With the introduction of voice calling becoming available in the next few months, at what is said to be free, potential add-ons to this feature are endless. Adaptations of the iPhone's FaceTime or extra emoticons at low prices will help create the revenue the company is needing and make the sum of $19bn seem a lot more reasonable. What most new users don't realise, like myself, is only the first year of WhatsApp is free. After 12 months your account will expire and you will be asked to pay prior to your subscription end date.

Mark Zuckerburg spoke on behalf of Facebook at a press conference in Barcelona yesterday and believes that WhatsApp is a "rare platform that has the potential to reach out to 1 billion mobile users". The real majesty of web dynamics and most obvious is the colossal global reach at nearly zero marginal costs. Whatsapp has around 50 employees. It has no marketing costs. No Washington lobbyists. No stores. No global campus. No sponsorship of the local symphony. With the introduction of voice calling becoming available in the next few months, at what is said to be free, potential add-ons to this feature are endless. Adaptations of the iPhone's FaceTime or extra emoticons at low prices will help create the revenue the company is needing and make the sum of $19bn seem a lot more reasonable. What most new users don't realise, like myself, is only the first year of WhatsApp is free. After 12 months your account will expire and you will be asked to pay prior to your subscription end date.

But what has Facebook really got to lose? Zuckerburg bought WhatsApp because it gives him a hook into hundreds of millions of customers, who may get shoved over to Facebook, and its ad platform, in ways even he's not dreamed of yet. As of yet Whatsapp is ad-free but who's to say they won't start displaying them on this platform? It's now in Facebooks hands to do what they like. There's been so little precedent for business at this scale that all we can do is wait to see what comes of it and if the takeover really was worth the price they've paid.